2001: A School Bond Odyssey

A series on budgeting, facilities planning, and what Laguna Beach should understand before 2026

Part 3: Laguna Beach Unified’s bond history, without the finance fog

Once I got into Laguna Beach Unified’s actual bond history, it became pretty apparent that much of the confusion is not really about disagreement. It is about vocabulary.

People throw around terms such as bond, series, refunding, and tax rate as if they all mean the same thing, or as if hearing one of them means the district is quietly doing something new behind the scenes. A lot of the time, that is just not true.

Before people start speculating about what a future bond might mean, it helps to understand what Laguna Beach Unified has actually done over the last 25 years. I would like to note that Proposition 39 was already available in 2001, as it had passed in 2000 to create the 55% path people are more used to hearing about now, but districts can still run a traditional two-thirds bond election instead. Laguna Beach Unified’s 2001 bond used the two-thirds route.

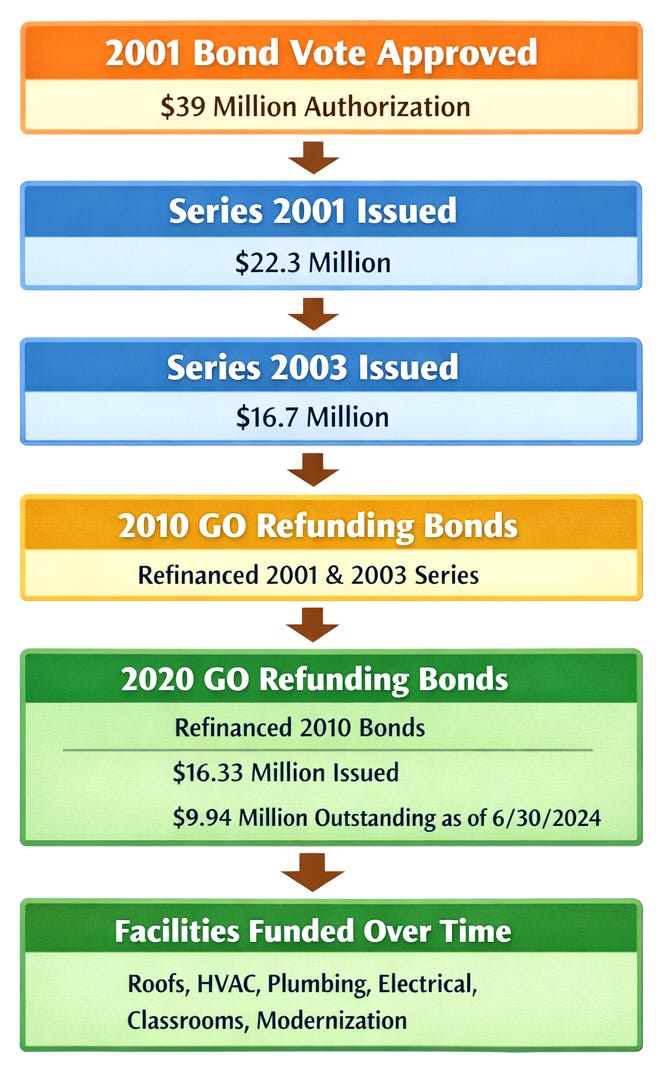

I found a pretty straightforward timeline: a $39 million GO bond authorization approved in 2001, two series issued under that approval, a refunding in 2010, another refunding in 2020, plus a separate Crystal Cove CFD history that people tend to lump in without explaining.

The GO bond Laguna Beach actually approved

The main local general obligation bond in this window was approved on June 5, 2001, when voters authorized $39 million in GO bonds for Laguna Beach Unified. It passed with about 80.36% in favor and was documented as a traditional two-thirds special-election bond, not a Proposition 39 bond.

That matters for a couple of reasons:

It shows there is already a local history here. This is not some brand-new financing idea suddenly appearing out of nowhere.

The 2001 bond did not come through the Prop 39 structure, which shows that not every school bond follows the same rules or comes from the same legal framework.

The documented purpose was what you would expect from a facilities bond: capital improvements and modernization, including the kind of work people rarely get excited about until it stops working, like roofs, electrical, plumbing, HVAC, and classrooms. In other words, the backstage systems.

One bond, more than one sale

This is where people tend to get lost, and honestly, it is also where a lot of sloppy shorthand takes over.

The bond measure was what voters approved in 2001, and it is the authorization.

The district did not necessarily borrow the full $39 million in one shot. Instead, that authorization was later issued in two separate bond series: Series 2001 for $22.3 million and Series 2003 for $16.7 million, issued by the County of Orange on behalf of the district.

A series is not a new vote or a “surprise” second bond. It is one actual sale under authority voters had already approved, and not evidence that the district quietly went back for more.

People hear “Series 2003” and assume it must refer to a new bond issued in 2003. It did not. It means the district was still drawing on the borrowing authority voters had already approved in 2001.

Districts do this because projects do not all move at once, and it usually makes more sense to borrow in stages than to take every dollar up front and pay interest on money that is not yet needed.

What changed later

Then comes the next word that gets people spun up: refunding. A refunding is basically a refinance. It is not the same thing as a new bond measure.

Laguna Beach Unified’s records state that on August 4, 2010, the district issued 2010 GO Refunding Bonds to refinance the earlier Series 2001 and Series 2003 bonds. Then in 2020, it refinanced again. The district’s June 2024 audit reports the outstanding GO debt as 2020 General Obligation Refunding Bonds, originally issued at $16.33 million, with $9.94 million still outstanding as of June 30, 2024.

This is not the district quietly stacking new debt on top of old debt. It is the district restructuring of existing debt.

In the 2020 case, the district conditioned the issuance on achieving at least 5% net present value debt service savings on the refunded bonds. This is exactly the kind of thing districts should be looking for when they refinance. The same documentation also notes that the 2020 bonds were sold competitively and refunded $18.135 million of the 2010 GO refunding bonds.

So again, the vocabulary matters:

A bond measure is a voter authorization. A series is one sale under that authorization. A refunding is a refinance of debt already issued.

Once those three things are separated, the local history stops sounding nearly as mysterious as people make it out to be.

What the bond has cost us (the taxpayers)

This is where the conversation usually gets oversimplified.

Laguna Beach’s school bond has not cost taxpayers today’s rate for its full life. At the time of the 2001 election, the district said the new bonds would cost about $36 per year per $100,000 of assessed value (if you paid $10,000 a year in property taxes, the bond cost $250).

This number did not stay fixed forever. Bond tax rates change over time depending on the amount of principal remaining, the debt's structure, whether it is refinanced, and how assessed values grow. In Laguna Beach Unified’s case, the later refundings are a big reason that today’s number looks so different from the original 2001 estimate.

That means there were some cost savings for taxpayers for the 2010 refunding, which refinanced the earlier 2001 and 2003 series. The 2020 refunding refinanced that 2010 debt, which Laguna Beach Unified estimated saved taxpayers $4 million.

By the time you get to the current period, the rate is much lower. Orange County tax-rate books show Laguna Beach Unified’s bond rate at $10.18 per $100,000 of assessed value in 2021-22, $9.71 in 2022-23, $8.83 in 2023-24, and $8.76 in 2024-25 (if you paid $36,000 in property taxes, the bond now costs cost $250).

This information will hopefully counter a lot of the lazy rhetoric around school bonds. The school bond authorization does not lock taxpayers into one flat number forever. Over time, assessed value growth and refundings substantially reduced the rate.

The separate Crystal Cove piece

There is also another piece of Laguna Beach school-related public finance that can muddy the waters if people are not careful.

Laguna Beach Unified has a separate Community Facilities District, CFD No. 98-1, tied to Crystal Cove. That is not the same thing as the district’s main GO bond. It is the Mello-Roos special tax debt, which follows a different structure. The district’s broader bond history summary explicitly treats the GO bond line and the Crystal Cove CFD line as separate financing tracks.

What I found is that this CFD had bond anticipation notes in 1999, special tax bonds in 2004, and special tax refunding bonds in 2012. The district’s reporting says the underlying purpose was still school-facility related in capital terms, including facilities, land and rights-of-way, planning and design, and environmental evaluation tied to mitigation obligations. As of June 30, 2024, the district reported $6.41 million in outstanding debt.

That is worth mentioning because people often collapse all district-related debt into a single bucket and then talk about it as if it were all the same thing. If someone is trying to explain Laguna Beach Unified’s debt picture without distinguishing between the 2001 GO bond history and the Crystal Cove CFD, they are leaving out an important part of the story.

What still gets twisted

This is probably the most frustrating part of this topic.

Once people decide they want to treat “bond” as a stand-in for “problem,” every related term starts getting bent in that direction too. “Series” becomes “more borrowing.” “Refunding” becomes “more debt.” Older authorizations are discussed as if they were fresh asks.

This is exactly why it is worth slowing down and naming things correctly. Not because the jargon is exciting, but because once terms get sloppy, the conversation gets more fractured right after them. And at that point, people are not really arguing about the district’s history anymore; they are arguing with a version of it that has already been flattened into a talking point.

Next up

So that is Laguna Beach’s school bond history in broad strokes.

Next, I want to get into what bond money actually turns into, what Laguna Beach facilities projects people can point to, what the master plan is doing in the background, and why that part of the story is usually easier to understand once the finance language is out of the way.

The Good, the Bad, & the Boring: School Bonds

Part 1: Why even a well-funded district still needs bonds